Storage for DBAs: There are many things you need to know about flash: it’s performance, it’s behaviour, it’s durability etc. But there’s one single piece of information which tells you more than anything else, because it gives you an insight into the future of not just flash memory, but the primary data storage industry. Let me explain, but first let me contrast against something we all more familiar with: disk drives.

Disk Drive Market History

Almost all disk drives are made by three manufacturers: Western Digital, Seagate and Toshiba. There used to be a lot more than that, but all the others either went out of business or got acquired. These are tough times for disk drive manufacturers, with sales expected to take a double-digit dive in 2013. It was not always this way though; for decades the thirst for HDDs was unquenchable, with large volumes of them being required in desktop PCs (remember them?) as well as enterprise disk arrays. Fast forward to the present day and desktop PCs have been ambushed by tablets and SSDs, while flash is now similarly disrupting the data centre.

For a minute though, let’s remember the golden era of disk. If we rewind around eight years ago, the disk industry was thriving. To quote a TrendFocus report published in Businesswire (emphasis added by me):

The industry’s 25% unit growth in 2005 was based on solid fundamentals in core markets like PCs and servers… Booming notebook PC sales caused a surge in 2.5″ HDD shipments to 77 million, a 45% growth. Enterprise HDD shipments grew 11% to over 26 million units. HDD industry revenue was $28 billion, an increase of 18% from 2004.

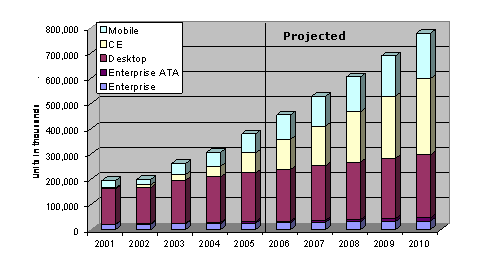

An 18% annual increase… that’s impressive! As the quote states, this growth was built on the “solid fundamentals” of PCs and Servers – nobody foresaw the end of the PC disk market, because a new and exciting range of “Notebook PCs” seemed ready to drive demand even higher. And on top of that, two new market segments were growing rapidly: Consumer Electronics and Mobile. The graph on the left was created in 2005 and showed HDD market predictions going forward until 2010. The yellow and light blue colours indicate CE and Mobile respectively – you can see that there was a lot of optimism for the future – while the reddish colour indicates the huge returns from desktop PCs (while the Enterprise segment is merely a small purple brick at the bottom of each column). But somewhere at the bottom of a 2005 Q4 report published later that year were the first indications of a changing tide:

Shipments accounted for slightly less than the 20 percent forecast, and the drop-off is attributed to Apple’s decision to move away from 1-inch-based hard drives for its iPod mini business.

What did Apple move to? Take a guess. Very slowly, but very surely, the potential CE and Mobile markets evaporated. At the same time, the Desktop PC business died a lingering death, leaving enterprise storage as the mainstay for hard drives.

That’s one thing which remained constant through this period though: the enterprise HDD market. Enterprise Storage vendors like EMC and NetApp bought up massive volumes of disk drives to put in enterprise class arrays for their customers – and these massive volumes meant two critical outcomes:

- The larger Enterprise Storage vendors bought at enormous discounts

- HDD vendors selling to Enterprise Storage focussed their R&D efforts on improving the characteristics that these customers desired

The characteristics required for enterprise storage were: density and performance. It’s a simple case of supply and demand. As with all business, the demand shapes the supply.

NAND Flash Market Forces

One thing that flash has in common with disk is the relatively small number of manufacturers. Note that I’m not talking about companies like Violin here, I’m talking about the flash chip manufacturers who own the fabs. In 2012 the NAND flash market consisted of Samsung (38%), Toshiba (28%) – the inventor of flash, Micron (14%) and Hynix (12%). But who was the largest buyer worldwide? Was it EMC? Netapp? IBM, HP or Dell?

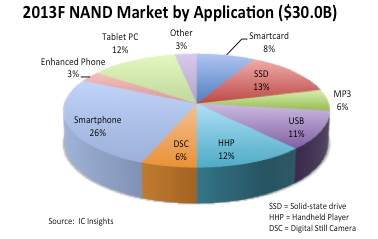

In 2011, Apple became the largest worldwide consumer of NAND flash. And as I’m sure you can guess, the reason for this was the iPhone. Today, according to IC Insights, the majority of NAND flash (59%) is used in smartphones, tablets and portable devices, with another 17% used in USB keys and cameras. If you look at the pie chart on the right, that little red portion marked SSD (just 13%) comprises all the flash used in both enterprise storage and consumer solid state drives (e.g. the ones you might get in an ultrabook).

And that trend is only going one way. By the end of 2013 it is forecast that there will be nearly 1.5 billion smartphones in the world – one smartphone for every five people. Meanwhile, tablets are not only the fastest growing segments but also one of the fastest-growing consumer devices of all time.

What does this mean? It means that NAND flash development is driven by the consumer market, by smartphones and portable devices. In enterprise storage, when we talk about flash we always talk about performance and endurance – but the consumer market isn’t interested in either of these. The consumer market is interested in density, i.e. how much data you can fit on a chip, as well as power consumption and cost. If a NAND flash manufacturer could produce larger flash chips at the cost of 20% slower performance, for example, this would be considered a great result. There’s a fundamental difference in requirements between the consumer and enterprise markets: only the enterprise cares about performance.

The Balance Of Power

In the heyday of disk, the enterprise storage industry had serious influence on what came out of the factories. But with NAND flash, the power of the enterprise storage industry to influence the direction of development is clearly far weaker. Sure there are relationships between flash storage vendors and the manufacturers – in fact, one of the strongest is between Violin and Toshiba – but market forces dictate that NAND flash development will be mostly influenced by the consumer market: the phone in your pocket and the tablet on your desk. (Don’t be confused by claims of “enterprise-class” NAND flash either – the key is to follow where the billions of dollars of R&D money are going, i.e. the consumer market. Enterprise-class flash is merely the least-consumer-like consumer flash…)

What does this mean for enterprise storage? It’s simple – it means that each enterprise vendor will have to take “consumer” flash and come up with innovative ways to make it perform like an enterprise product. Each flash vendor needs to do this to deliver the performance you need. Anybody can take a bunch of flash cards or SSDs and put them in a box, but that’s not innovation. The flash vendors who survive the great flash market consolidation will be the ones with intellectual property and patents around making consumer NAND flash perform for the enterprise.

Understand this and you will know the most important thing to ask a potential flash vendor about their product is not “How fast is it?”, or “How long does it last?”, but “Where’s your innovation?”. After all, if your vendor isn’t adding anything to the equation, you might as well be doing it yourself…

This article is part of the Storage for DBAs series. If you found this series useful, you might also be interested in Databases in the Age of AI, which examines how AI agents are now placing enterprise systems of record under a new kind of pressure.

Hi,

Very interesting topic. Any chance you elaborate further regarding “Where’s your innovation?”. If flash improvements is not driven by flash storage vendors, what are the different alternatives on which flash vendors can differentiate their products ?

Thanks !

Olivier

All in good time my friend 🙂

I have articles queued up to explain a) the issues which vendors need to overcome, and b) the methods used by Violin to overcome them.

The point is to consider whether the vendor you speak to is doing anything innovative (which basically means patented) or whether they are just shoving some flash in a server and calling it an array…

Can’t wait 🙂 You know, your blog series about storage is the most fresh and up to date i’ve ever read. This is invaluable stuff for Oracle dbas, but not only. So again thank you very much [all this stuff really deserves a huge whitepaper and is obviously the perfect stuff for a presentation at any OUG annual conference].

Thanks! 🙂 You’re flattering me. But there are other bloggers out there covering I/O topics really well – James Morle for example.

Still, it’s good to hear from readers. It helps inspire me to stop being lazy and write more. Storage is going to change drastically over the next few years and DBAs need to be prepared.

Its an interesting piece…..inovation is great BUT sometimes the easy option, to do the easy thing, is “good enough” and that is why those vendors will still sell lots of “flash arrays”….

The enterprise flash marketplace has been through a massive growth period and there are now too many players to survive the coming consolidation. Those who have no innovation to offer – no Intellectual Property or patents – will be the first to disappear.